Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Published: January 31, 2024

Updated: January 31, 2024

The $ 28 billion Indian cement industry is on a roll. Churning out 310 million tonnes and ranking as the world’s second largest cement producer, the country’s cement sector has played an important role in the nation’s development since independence.

The infrastructure sector is crucial to the country’s economic growth. The British left India in 1947 as an under-developed country in dire need of a comprehensive infrastructural base. After all, it is infrastructure which fosters the expansion of a variety of industries, such as real estate and public utilities. A growing construction industry feeds off the rising need for urban dwellings and powers the production of cement, thus boosting the Indian cement market. The infrastructure sector includes utilities, bridges, dams, roads and urban facilities. And the cement industry is key to achieving these and other objectives.

Needless to say, there has been significant growth in the cement sector in recent years, and the trend is expected to continue going ahead. Reflecting the sustained growth of the industry, cement stocks have started stealing the limelight.

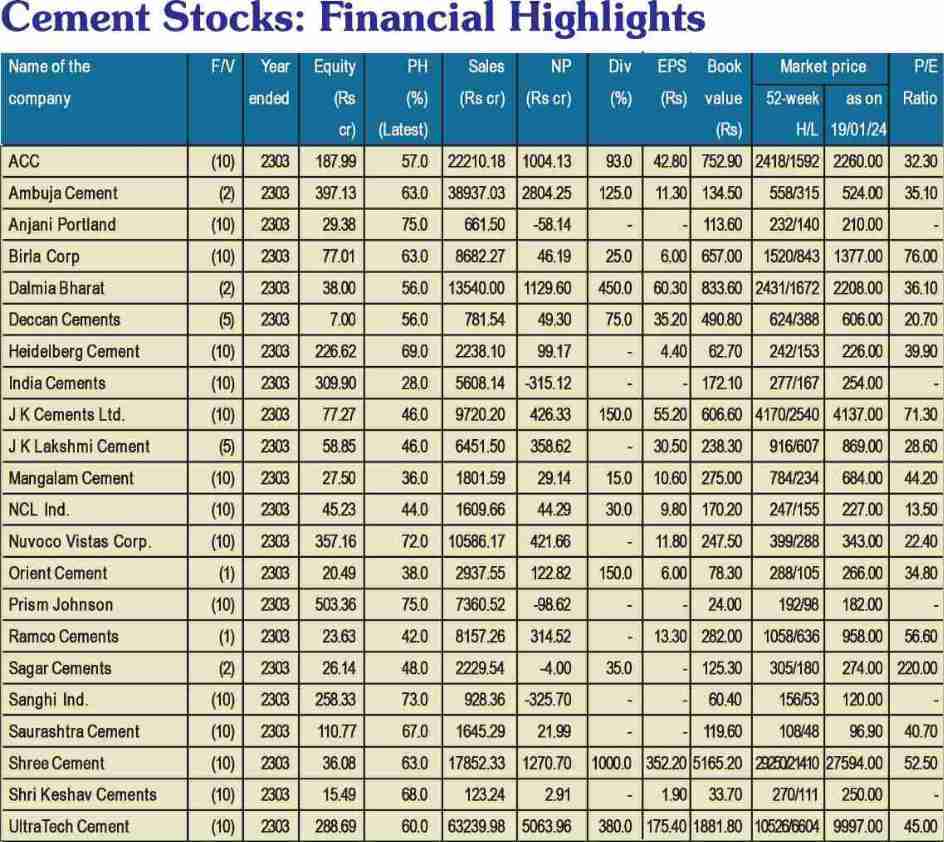

Ultratech Cement, originally created by engineering colossus Larsen & Toubro and subsequently acquired by Kumar Mangalam Birla of the Aditya Birla group, whose shares have a face value of Rs 10, crossed a historic high of Rs 10,000 before settling around Rs9,834. Ramco Cements which had gone up to Rs 636 (FV Re 1) last year, has shot up further to Rs 1,058 before rereating to Rs 941. ACC, which was friendless in 2000 around Rs 84 and had climbed to Rs 1,593 early last year, has risen further to Rs 2,400 before coming down to Rs 2,202 at present.

Ambuja Cement, which was available around Rs 93 in 2008, shot up to Rs 315 early last year and has now spurted to Rs 525. JK Cement, which had no takers around Rs 35, surged to Rs 2,542 early last year and is at Rs 3,949 at present.

Dalmia Bharat, with a face value of Rs 2, which was quoted around Rs 406 in 2020 and climbed to Rs 1,675 earlier last year, has climbed further to Rs 2,110. RHI Magnista India, formerly known as Orient Refractories, with a face value of Re 1, has surged from Rs 576 early last year to Rs 870 before quoting around Rs 728.

Interestingly, almost all cement stocks are currently quoted at sky-high levels and continue to attract inquiries and demand from investors.

With India’s growing population and extensive infrastructural development, cement demand has been continuously on the rise. According to IBEF statistics, this upward trend is projected to persist, with consumption expected to reach 600 million tonnes by 2025. The need for residential, commercial and industrial development drives this surge in demand.

Again, the construction of multimodal transport networks of world-class quality, including more than 100 Smart City projects, will further boost the cement industry.

Comments an expert on the cement industry, “New Delhi’s commitment to ambitious projects such as the National Infrastructure Protection Plan (NIPP) and the Bharatmala road projects are leading to a substantial demand for cement.” These initiatives aim to enhance the country’s transportation network, including highways and roadways, necessitating large quantities of cement for construction. The Pradhan Mantri Awas Yojana (PMAY), with its urban and rural components, is a crucial driver for the Indian cement market. PMAY aims to provide affordable housing to all citizens, aligning with the government’s vision of ‘Housing for All’. The construction of millions of housing units under this scheme has led to a substantial demand for cement, particularly as the country is undergoing rapid urbanisation with an increasing percentage of the population migrating to urban areas.

According to projections, 39 per cent of India’s population is expected to reside in urban areas by 2030, compared to the current 35 per cent. Urbanisation entails the construction of residential and commercial infrastructure, leading to a surge in demand for cement in various construction projects. The average size of the Indian household has been decreasing from 5.3 members in 2011 to 4.6 members in 2019, and this has gone further down to 3.6 in 2024. This shift towards smaller households is a noteworthy driver for the Indian cement market. Smaller houses result in the construction of more residential units to accommodate the growing population, translating into a consistent demand for cement.

The Indian cement industry has made rapid strides in size and stature in recent years, particularly after the shackles of controls were removed. Today there is a total of 210 large cement plants, out of which 77 are in Andhra Pradesh, Rajasthan and Tamil Nadu. The installed capacity, which was around 390 million tonnes with actual production being 270 million tonnes in 2014-15, expanded to an installed capacity of 460 million tonnes in 2019-20. The industry is expected to sustain its fast-paced growth and attain an installed capacity of 850 million tonnes by 2030 and 1,350 million tonnes by 2050.

Not only in size, the industry has made tremendous strides in technological upgradation and assimilation of the latest technology. At present, about 99 per cent of the total capacity in the industry is based on the modern and environmentally-friendly dry process technology. Continuous modernization and technology upgradation with state-ofthe-art technology is being pursued by the industry to achieve improved energy, environment and quality standards.

Single production line capacity of over 12,?000 t/d with multi-stream preheaters and calciners; average thermal energy consumption of 726 kcal/kg (3037 GJ/t) clinker or average electrical energy consumption of 78 kWh/t of cement, as at present, were unimaginable two decades ago, when these figures hovered around 3,000 t/d, 880 kcal/kg (3682 GJ/t) clinker and 120 kWh/t of cement respectively. The best levels of thermal and electrical energy consumption achieved by the industry, namely 686 kcal/kg (2870 GJ/t) clinker and 68 kWh/t cement are comparable with the best in the world. Presently, cement companies in India are building global capacities, modernizing plants, improving efficiencies, cutting costs and restructuring their business houses to become highly competitive.

The technical innovations and constant modernization in mills, separators, calciners, burners, coolers, fans and air pollution control equipment have been chiefly responsible for such a phenomenal increase in capacity of single production lines as well as reduction in energy consumption and particulate emissions. The guide norms for cement plant operations developed by the NCB have also helped the industry in India to set up benchmarks for effective monitoring and improvement of operational efficiency.

Operating costs have been inflationary over the last decade. Energy related costs - coal, power and freight -- constitute nearly 55-60?% of the industry's operating costs. In this scenario, cogeneration of power, a relatively recent initiative in the Indian cement industry, is expected to find wider application across the industry in future. 15 cement plants have successfully implemented it and have installed 200 MW of cogeneration capacity. The industry potential of co-generated power is estimated to be more than 600 MW. The Indian cement industry is also setting up power generation units using renewable forms of energy like solar and wind energy.

The Indian cement industry has shown phenomenal performance in terms of environmental protection. Plants have adopted various measures to reduce stack as well as fugitive particulate emissions. The Indian cement industry is also highly eco-friendly. More than 17 million trees have been planted in the last decade, which could act as a carbon sink. Abandoned mines have been turned into water reservoirs, with rain water harvesting and recreation sites.

Needless to say, with the sustained growth of the industry, cement companies have also have put up a robust performance. A remarkable aspect of this growth is the trend to achieve controlling power in the market by expanding their ownership through organic expansion and inorganic acquisitions. Though there are 210 large cement plants in the country, a few industrial groups, headed by the Aditya Birla group, have been dominating the market. Now, the Adani group has entered the scene by acquiring ACC and Ambuja Cement and is setting up new plants in Chhattisgarh to expand its cement capacity. An unhealthy outcome of this trend is the formation of cartels to jack up selling prices at their whims and fancies.

As cement companies have been doing very well in their financial performance, their stocks have also started scaling new high levels, some of which are totally unexpected. The industry is doing very well and it is prospects going ahead are highly promising. We have picked some cement stocks which are worth investing in. Here goes the list. Happy investing.

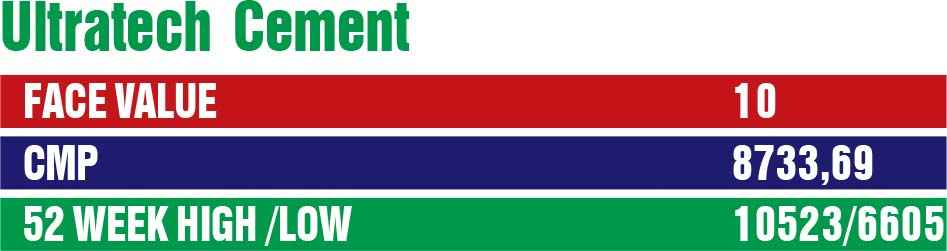

Ultratech Cement, the largest cement manufacturing company in the country, is the cement flagship company of the Aditya Birla group headed by Kumar Mangalam Birla, the uncrowned king of the cement industry in India. A $ 70 billion building solutions powerhouse, Ultratech is one of the leading players in the white cement segment in India and is also the third largest cement producer in the world, excluding China. The company's business operations span the UAE, Bahrain, Sri Lanka and India.

With 23 integrated manufacturing plants, 29 grinding units, one clinkerisation unit and 8 bulk packaging terminals, Ultratech is the only cement company in the world (outside China) with 100+ mtpa of cement manufacturing capacity. In order to move towards achieving its target of 200 mtpa capacity, the company has acquired the cement business of Kesoram Industries.

The company's building products business is an innovation hub that offers an array of scientifically engineered products to cater to new-age constructions.

The company has gone from strength to strength on the financial front. During the last 12 years, its sales turnover has more than trebled from Rs 18,351 crore in fiscal 2012 to Rs 63,240 crore in fiscal 2023, with operating profit moving up from Rs 4,194 crore to Rs 10,620 crore and the profit at net level inching up from Rs 2,389 crore to Rs 5,072 crore. Ultratech's financial position is extremely sound, with reserves at the end of March 2023 standing at Rs 50,030 crore - over 186 times its equity capital of Rs 289 crore. The company is reducing its debt, with the interest burden coming down from Rs 1,992 crore in fiscal 2020 to Rs 823 crore in fiscal 2023.

The Ultratech stock is a favourite of research analysts, institutional investors and high net worth investors. The Rs 10 face value stock had climbed Himalayan heights of Rs 10,523 before settling around Rs 9,834. Prospects for the company are robust going ahead. The Bangur group-owned Shree Cement is one of the 2 leading cement groups in India with a cement production capacity of 50.4 mtpa and a power generation capacity of 771 MW. Since its inception in 1979, the company has been on a sustainable and inclusive growth path with its consistent pursuit of innovation and operational excellence.

Since inception, the company has grown steadily to emerge as one of the top cement companies in the country and one of India's most cost-efficient cement producers. Shree Cement's Navalgarh cement plant has gone on stream. According to Dow Jones, the plant has an integrated cement capacity of 4.2 million tonnes per year. The company has accelerated its growth plans and outlined expansion plans of 12 mtpa at a capex of Rs 70 billion. This along with the ongoing plans will increase company's capacity to 72.4 mtpa. It plans to achieve a capacity of 80 mtpa in the next few years.

The company has been performing very well on the financial front. During the last 12 years, its sales turnover has been trebled from Rs 5,641 crore in fiscal 2012 to Rs 16,837 crore in fiscal 2023, with operating profit inching up from Rs 1,646 crore to Rs 2,942 crore and the profit at net level more than doubling from Rs 618 crore to Rs 1,328 crore. The company's financial position is very strong, with reserves at the end of March 2023 standing at Rs 18,252 crore - over 507 times its equity capital of Rs 36 crore. The company's stock is the most expensive cement stock in the country. The share with a face value of Rs 10 is quoted around Rs 27,954. This can be a good addition to the portfolio of investors with a long-term perspective.

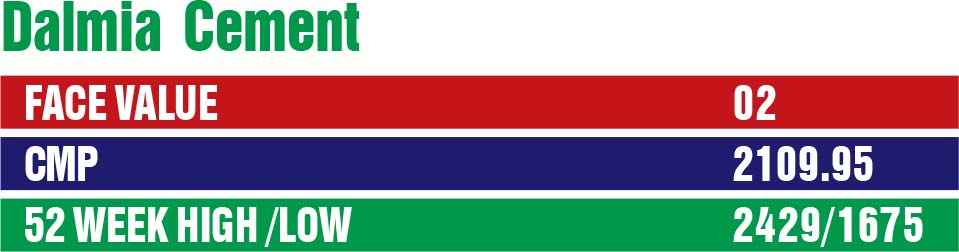

Over eight decades old, Dalmia Bharat is among the top five cement companies in the country with a strong presence in 22 states, serving clients through an extensive network. It has a total capacity of 35 million tonnes per annum, with its current capacity mix spread at 59 per cent in the east, 33 per cent in the south and 8 per cent in the west.

The company is growing steadily in its financial performance. During the last 12 years, its sales turnover has almost doubled from Rs 7,444 crore in fiscal year 2012 to Rs 13,540 crore in fiscal 2023, with operating profit moving up from Rs 1,894 crore to Rs 2,316 crore and the net profit shooting up two and a half times from Rs 44 crore to Rs 1,079 crore. The company's financial position is very strong, with reserves at the end of March 2023 standing at Rs 15,973 crore - over 400 times its equity capital of Rs 38 crore. With a steady cash flow, the company has been able to reduce its borrowings from Rs 8,038 crore in fiscal 2017 to Rs 3,855 crore in fiscal 2023, enabling the company to reduce its interest burden from Rs 856 crore in FY2017 to Rs 234 crore.

With a view to expanding its size and stature, it has now decided to acquire Jaypee Cement, a part of Jaiprakash Associates. The deal's cash outflow is earmarked at around Rs 3,300 crore. According to the deal, which is slated to be completed by March 2024, Dalmia Bharat will acquire Jaypee's plants situated in Uttar Pradesh, Madhya Pradesh and Chhattisgarh at a total cost of Rs 5,500 crore.

The acquisition is expected to give Dalmia Bharat a strong foothold in central India, which accounts for 15 per cent of the country's cement demand. Again, Dalmia Bharat's capacity will be now more diversified with 52 per cent in the east, 26 per cent in the south, 16 per cent in the central India and 6 per cent in the west.

In the current boom period, the stock price of Dalmia Bharat has shot up from the 52-week low of Rs 575 (face value Rs 02) for Rs 2,429 before settling around Rs 2,110. The acquisition of Jaypee Cement is expected to brighten the prospects of the company going ahead. Starting with a small plant in Nimbahera, situated in Chittorgarh district of Rajasthan, with a capacity of 3 lakh tonnes per annum in 1975, JK Cement, belonging to the well-known industrial JK group, has emerged today as a leading cement company producing high-quality cement with several plants located at Golan (Rajasthan), Muddapur (taluka Mudhol in Bagalkot district of Karnataka), Jhajjar (Haryana), Aligarh (UP), Balasinor (Gujarat), Katni (Madhya Pradesh), Ranna (Madhya Pradesh), Aamirpur (Uttar Pradesh) and Fujiara (the Middle East), among others. The company was the first to produce white cement in the country.

The company is known for the high quality of its cement. At its Golan white cement plant, it uses the technical expertise of FL Smidh & Co. from Denmark and stateof-the-art technology with continuous on-line quality control by micro-processors and x-rays to ensure that only the purest white cement is produced. The company manufactures white Portland cement through these 5 significant stages - crushing, raw meal grinding, clinkerisation, cement grinding mill, crushed limestone. Clays and feldspar are fed through electronic weigh feeders.

The company has done very well on the performance front. During the last 12 years, its sales turnover has expanded by around three and a half times - from Rs 2,545 crore in fiscal year 2012 to Rs 9,720 crore in fiscal 2023 with operating profit moving up from Rs 514 crore to Rs 1,327 crore and the profit at net level inching up from Rs 175 crore to Rs 419 crore.

In the current boom period for the cement industry, the stock price of JK Cement has advanced from the 52-week low of Rs 2,542 to Rs 4,240 before settling around Rs 4,171. Prospects for the period going forward are quite promising. Discerning investors can certainly accumulate these stocks at every decline. Established in 1936, ACC (Associated Cement Companies) is one of the oldest cement companies in the country and is synonymous with cement. Originally belonging to the Tatas who sold it to the Holcim group of Switzerland, it has been acquired now by the Ahmedabad-based Adani group in 2022. The company produces a wide range of cement products and has demonstrated consistent financial growth.

During the last 12 years, the company's sales turnover has more than doubled form Rs 10,153 crore in calendar year 2011 to Rs 22,210 crore in fiscal 2023, but it fared poorly on the profitability front with operating profit remain static - from Rs 1,921 crore to Rs 1,925 crore and the net profit declining from Rs 1,301 crore to Rs 885 crore. However, the company has staged a remarkable turnaround during the last 12 months. With recent capacity addition, it's total cement capacity has gone up to 77.4 million tonnes per annum. This has enabled the company to push up volume, revenue and profitability growth on a substantial basis.

This year has seen a demand surge from the housing and infrastructure sectors, further aided by the government's spending push. Helped by capacity expansion, demand surge and price hikes, the company put up a scintillating performance during Q3 FY2024 (from October to December 2023), and its net profit shot up nearly five-fold to Rs 5,270 crore. This followed an 8 per cent spurt in revenues to Rs 49,180 crore which was helped by a 17 per cent yoy growth in cement and clinker sales volumes.

Future prospects for the company are all the more promising. According to the management, "Going ahead, cement demand in India will continue to grow at 7-8 per cent primarily fuelled by investments in infrastructure and largescale residential housing projects."

As a result, ACC shares surged 14 per cent to hit a 52- week high of Rs 255 before settling around Rs 2,207. As these shares have entered a bullish mode, future prospects are quite healthy.

July 15, 2026 - First Issue

Industry Review

VOL XVII - 10

July 01-15, 2026

Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Lighter Vein

1 Year *

Subscription

Rs 1800 /-

3 Year *

Subscription

Rs 5000 /-

5 Year *

Subscription

Rs 8000 /-

5

International

Subscription

$ 99.99

Read Corporate India and add to your Business Intelligence

Popular Stories

A modern-day enigma and a ramification of humanity's never-ending advancements, e-waste refers to the scum con- cealed by the outward glow of ever-advancing technology.

Archives

Office Address

Unit No. 405, 4th floor, Madhu Industrial Park, Avadh Narayan Tiwari Marg, Mogra Village Road, Andheri (East), Mumbai – 400069.

Call/Whatsapp

If you are interested in advertising with Corporate India, please don't hesitate to contact us. Our team is here to assist you with the process and answer any questions you may have. We look forward to the opportunity to work with you and help your business reach its full potential.

Fill out the form below to subscribe to our newsletter and never miss an update