Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Published: March 15, 2025

Updated: March 15, 2025

Is it advisable to recommend a Fortune Scrip at a time when the stock market is passing through a bear phase? Undoubtedly, market sentiment has been hit hard by adverse national and international devel opments leading to slowing down of economic growth at home, rising inflation, the manufacturing sector losing steam, growing unemployment, and declining urban as well as rural consumer demand.

As if these domestic factors were not enough, US President Donald Trump has administered a body blow to the Indian economy by threatening to impose stiff tariffs on Indian products entering the US. This threat adds to the uncertain global geopolitical situation. Little wonder then that the stock market has tumbled under widespread selling pressure led by foreign institutional and portfolio investors.

But our thinking is that if there are solid scrips with robust fundamentals and bright prospects, why should we not draw the attention of our readers to them? As a precautionary measure, we would advise waiting for a further fall in prices before picking such promising scrips. With this in mind, we have picked Jupiter Wagons as the Fortune Scrip for this fortnight.

Kolkata-headquartered Jupiter Wagons is the leading railway wagon manufacturer in the coun try. Over the past few decades, it has emerged as a one-stop solutions provider within its sector for coaches and alloy steel castings for rolling stock and track. The group also manufactures other products like ISO marine containers and refrigerated containers. Its wholly-owned subsidiary, Jupiter Electricity Mobility, is engaged in the manufacture of commercial electric vehicles. The group also manufactures gears and railway couplers for the Indian Railways and North American roads.

Today, Jupiter Wagons is the most integrated railway engineering company catering to clientele spread across the Indian Railways, private wagon aggregators, commercial vehicles, OEMs, and Indian defence logistics companies, among others. It regularly exports to North American markets as well.

The company’s major customers include Tata Motors, Reliance Industries, Ashok Leyland, Force Motors, Volvo Eicher Commercial Vehicles, Bharat Benz, Larsen & Toubro, BHEL, Indian Railways, Ministry of Defence, NTPC, Avia Motors, WP World, Container Corporation of India, and Adani Port and Logistics.

It is widely respected for its high quality and robust technology, which underpin its status of the fastest growing company in its space. One of the major factors for this achievement is that the company has tie-ups with world-renowned companies known for their top technologies. For ex ample, it has joined hands with DAKO-CZ of the Czech Republic for the manufacture of axle mounted disc brake systems for LHB passenger coaches. For the manufacture of brake discs for LHB coaches, it has entered into a joint venture with Kovis DOO of Slovnia. And in order to manufacture flash butt welded CMS crossings for the Indian Railway, it has entered into a JV with Talleres Alegutta sa of Spain.

The company has state-of-the-art manufacturing facilities at Kolkata, Jamshedpur, Indore, Jabalpur and Aurangabad, with complete backward integration of its foundry operations.

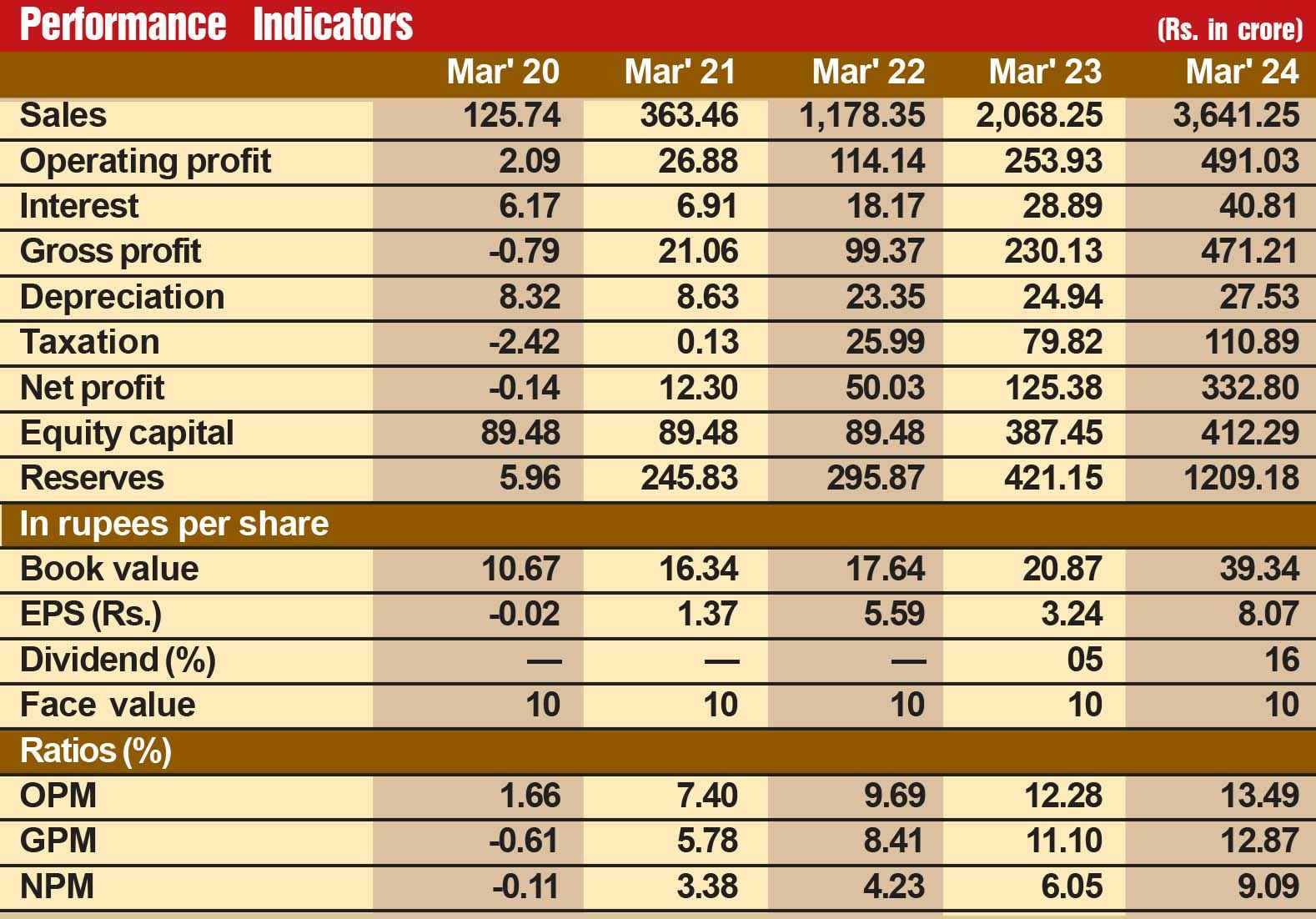

Jupiter Wagons has gone from strength to strength on the financial front, with sales and earn ings expanding over 7 times each. While sales during the last 12 years has expanded from Rs 502 crore in fiscal 2013 to Rs 3,641 crore in fiscal 2024, operating profit has grown from Rs 65 crore to Rs 491 crore and the net profit has expanded from Rs 19 crore to Rs 333 crore. But this robust performance so far is not the only reason why we have picked Jupiter as the Fortune Scrip. We strongly feel that its future prospects are all the more promising. Consider:

The company’s shares with a face value of Rs 10 are quoted around Rs 315 in the current bearish phase. As the domestic and international factors are highly disturbing, the share price may decline further to around the 240/250 level. Discerning investors will do well to wait for some time and then start accumulating these shares at every decline. The long-term outlook for this stock is distinctly bullish. Investors who invest in this stock with a long-term perspective will certainly reap a rich harvest.

May 31, 2026 - Second Issue

Industry Review

VOL XVII - 09

May 16-31, 2026

Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Lighter Vein

1 Year *

Subscription

Rs 1800 /-

3 Year *

Subscription

Rs 5000 /-

5 Year *

Subscription

Rs 8000 /-

5

International

Subscription

$ 99.99

Read Corporate India and add to your Business Intelligence

Popular Stories

A modern-day enigma and a ramification of humanity's never-ending advancements, e-waste refers to the scum con- cealed by the outward glow of ever-advancing technology.

Archives

Office Address

Unit No. 405, 4th floor, Madhu Industrial Park, Avadh Narayan Tiwari Marg, Mogra Village Road, Andheri (East), Mumbai – 400069.

Call/Whatsapp

If you are interested in advertising with Corporate India, please don't hesitate to contact us. Our team is here to assist you with the process and answer any questions you may have. We look forward to the opportunity to work with you and help your business reach its full potential.

Fill out the form below to subscribe to our newsletter and never miss an update