Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Published: November 15, 2025

Updated: November 15, 2025

With the stock market unnerved by national and global uncertainties, stock prices have been dawdling aimlessly with a downward inclination. And with the US dollar getting stronger by the day and the rupee steadily losing ground, foreign investors have been inclined to unload their holdings. Moreover, taking a cue from dishonest market operators, unscrupulous promoters are playing dirty games.

In these circumstances, selecting a Fortune Scrip becomes a challenge. In order to protect the interests of our readers, we did a good deal of searching and found a small-cap scrip with strong fundamentals and sustained growth prospects. Not many investors may be familiar with the name – it is south-based Hariom Pipes Industries.

Mehboobnagar (Telangana)-headquartered Hariom Pipes is a vertically integrated leading manufacturer of a wide range of iron and steel products, including various types of pipes, tubes and coils, scaffolding, HR strips, MS billets and sponge iron. The company uses iron ore to produce sponge to manufacture its final products — MS pipes and scaffolding — making the manufacturing process cost-effective. In fact, Hariom is one of the lowest-cost producers of MS pipes in the country.

According to our research, the company is poised for an exceptional growth trajectory, fuelled by a ramp-up in capacity, accelerated galvanised product sales via an established and extensive dealer network mainly in northern and western India, and favourable industry dynamics. Its backward integrated model stands as a testament to its strategic execution and is primed to scale effortlessly with rising capacities. Its tandem mill further strengthens Hariom’s market edge of production of sub-2 mm pipes – a true differentiator. With a turbocharged combo of an improving cash conversion cycle, rising return ratios, debt-to-equity metrics and resilient margins, Hariom is all set for robust growth and we strongly feel that the small-cap (equity capital Rs 31 crore) stock is poised for a re-rating as soon as the uncertainties in the market environment start declining.

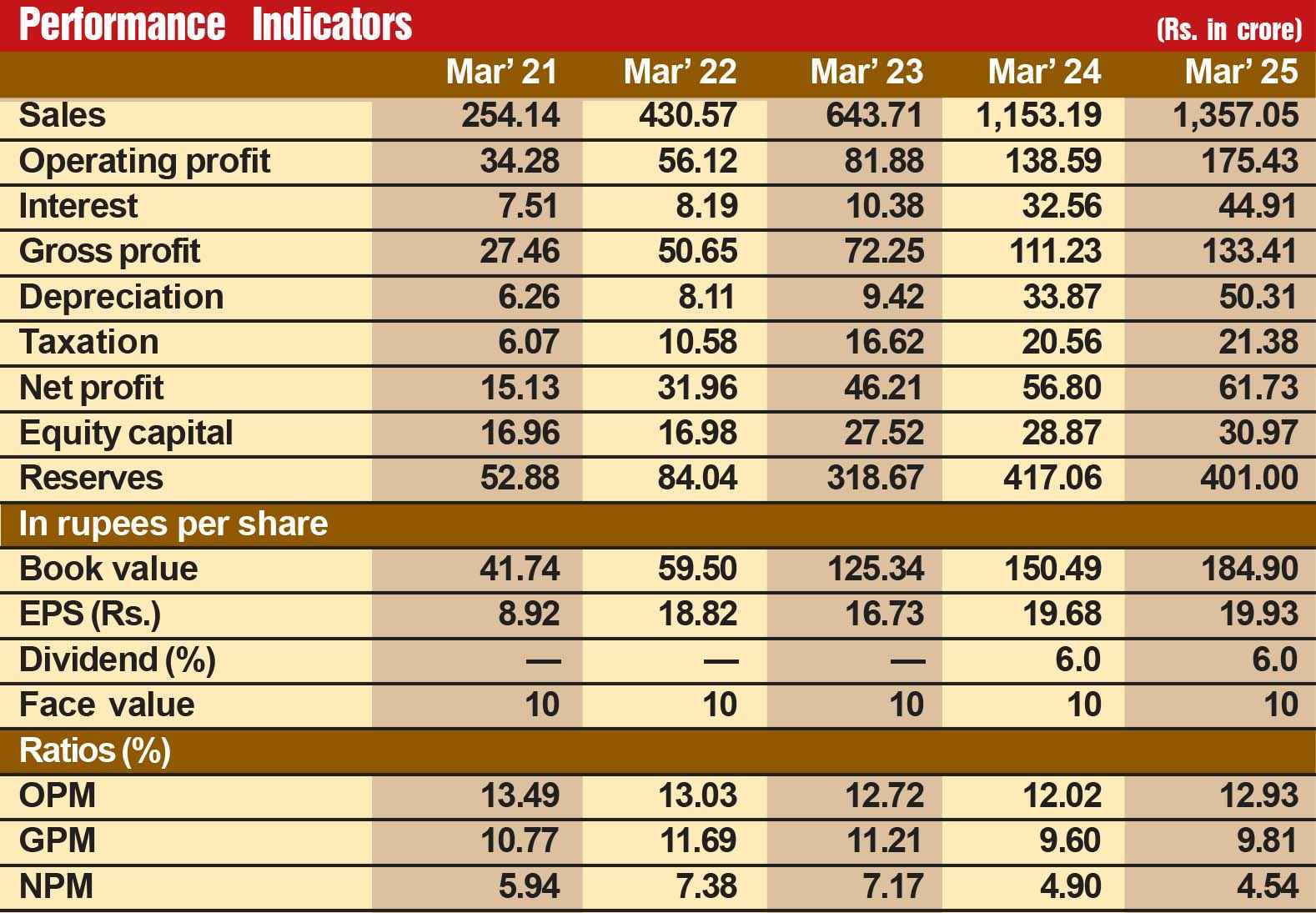

Despite a challenging market situation, Hariom is going from strength to strength in its financial performance. During the last 10 years, its sales turnover has continuously risen from Rs 87 crore in fiscal 2017 to Rs 1,604 crore in fiscal 2025, suggesting a spurt of over 18 times. In the same period, its operating profit has spurted 25 times from Rs 7 crore to Rs 175 crore, with the profit at net level shooting up 31 times from Rs 2 crore to Rs 62 crore. The company’s financial position is also very strong, with reserves at the end of March 2025 standing at Rs 574 crore — over 18 times its equity capital of Rs 31 crore.

But we have not selected this company as the Fortune Scrip only on account of its laurels so far. We are confident that Hariom’s prospects are robust going ahead, once the challenging market environment comes to an end. Consider:

The company's future prospects are highly promising. For the next two years, it has targeted a 30% volume CAGR. Its focus on value-added projects and strategic expansion positions it well for strong growth in the coming years. With capacity expansion, market reach, and entry into the renewable energy sector, the company is poised to capitalise on the growing demand for steel products in India's infrastructure and construction sectors. Its emphasis on sustainability and operational efficiency is likely to contribute to its long-term growth and profitability. In the current bearish phase in the stock market, the Hariom stock is quoted around Rs 368. Discerning investors with a long-term perspective should take a chance and invest in the stock, which we are confident is all set for rerating.

July 15, 2026 - First Issue

Industry Review

VOL XVII - 10

July 01-15, 2026

Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Lighter Vein

1 Year *

Subscription

Rs 1800 /-

3 Year *

Subscription

Rs 5000 /-

5 Year *

Subscription

Rs 8000 /-

5

International

Subscription

$ 99.99

Read Corporate India and add to your Business Intelligence

Popular Stories

A modern-day enigma and a ramification of humanity's never-ending advancements, e-waste refers to the scum con- cealed by the outward glow of ever-advancing technology.

Archives

Office Address

Unit No. 405, 4th floor, Madhu Industrial Park, Avadh Narayan Tiwari Marg, Mogra Village Road, Andheri (East), Mumbai – 400069.

Call/Whatsapp

If you are interested in advertising with Corporate India, please don't hesitate to contact us. Our team is here to assist you with the process and answer any questions you may have. We look forward to the opportunity to work with you and help your business reach its full potential.

Fill out the form below to subscribe to our newsletter and never miss an update