Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Published: March 15, 2026

Updated: March 15, 2026

For this fortnight, we have selected DCX Systems – one of the fastest-growing Indian companies in the field of system integration and cable & wire harnessing – as our Fortune Scrip. The Bangalore-based company has a reputation for customising its services to match the needs of its many clients at home and abroad. Its offerings span the entire spectrum of strategic defence and aerospace electronics systems, subsystems, and cable & wire harness assemblies.

The company’s system integration services encompass electronics and electro-mechanical assemblies in areas such as radar systems, sensors, electronic warfare, missiles and communication systems. These services are crucial to in-house quality services such as vibration and environmental stress testing of complex RF products utilised in radar communications, surveillance and missile systems.

System integration (SI) services constitute a comprehensive array of electronics and electromechanical assembly and services. DCX also provides product repair support for the parts it manufactures. As such, it is unique among listed companies for offering SI services to OEMs.

Originally, DCX started as an Indian offset partner (IOP) for foreign OEMs, primarily generating revenue as an IOP for Israel. Now its work spans India, the US and South Korea.

The company operates through a modern manufacturing facility spread over 30,000 sq ft at Defence and Aerospace Park in Bangalore, and has an in-house environment and electrical testing & wire processing facility.

DCX has partnered with Israel Aerospace Industries (IAI) to form a joint venture styled ELTX Systems, which focuses on developing advanced defence systems, including airborne radars and ground-based technologies for India's armed forces. It aims to bolster India's self-reliance by enabling local manufacturing and enhancing indigenous technologies.

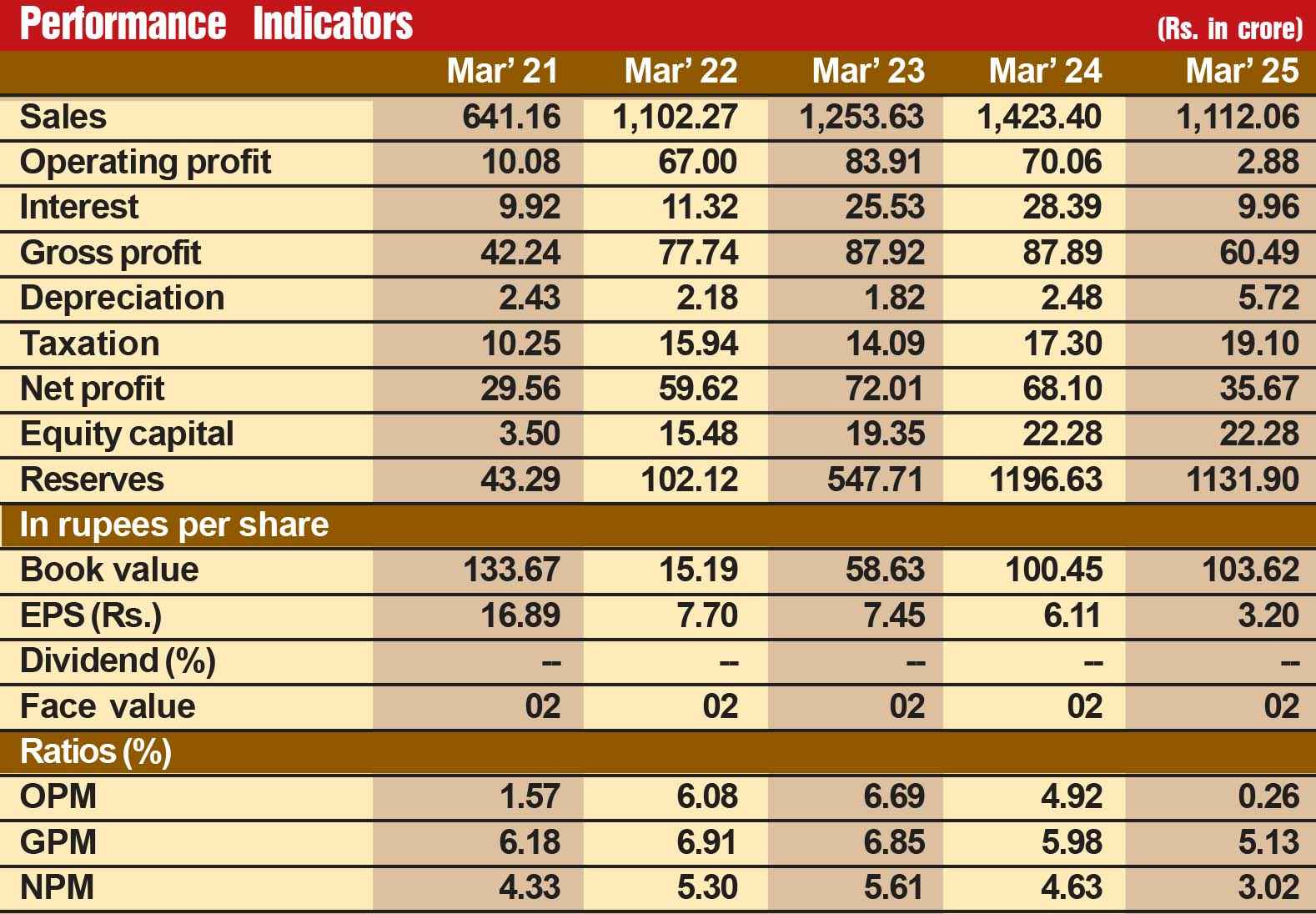

The company was doing exceedingly well till fiscal 2019, when sales declined to Rs 300 crore. In fiscal 2024, it put up an excellent show with sales spurting more than four and a half times to Rs 1,424 crore, operating profit shooting up more than 15 times from Rs 5 crore to Rs 80 crore, and the profit at net level jumping over 15 times from Rs 5 crore to Rs 76 crore.

However, during fiscals 2025 and 2026, the company has performed badly, with sales in fiscal 2025 falling to Rs 1,086 crore, operating profits tumbling to Rs 5 crore and net profit declining to Rs 39 crore. If the actual performance in the first three quarters of fiscal 2026 (April to December 2025) is any indication, its performance will continue to be dismal. Little wonder then that the share price has nosedived from the all-time high of Rs 452 (face value Rs 2) on July 3, 2024 to Rs 170 recently.

However, we are optimistic about the company as prospects for the defence and aerospace sector - to which DCX belongs - are highly promising, viewed in the context of fast-growing geopolitical tensions globally. Though the company's current performance is disappointing, its long-term prospects are highly encouraging. We admit that the share price, which has plunged to Rs 170, may fall further by 5-10 per cent, but we strongly feel that the stock is worth accumulating at every decline. Consider:

May 31, 2026 - Second Issue

Industry Review

VOL XVII - 09

May 16-31, 2026

Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Lighter Vein

1 Year *

Subscription

Rs 1800 /-

3 Year *

Subscription

Rs 5000 /-

5 Year *

Subscription

Rs 8000 /-

5

International

Subscription

$ 99.99

Read Corporate India and add to your Business Intelligence

Popular Stories

A modern-day enigma and a ramification of humanity's never-ending advancements, e-waste refers to the scum con- cealed by the outward glow of ever-advancing technology.

Archives

Office Address

Unit No. 405, 4th floor, Madhu Industrial Park, Avadh Narayan Tiwari Marg, Mogra Village Road, Andheri (East), Mumbai – 400069.

Call/Whatsapp

If you are interested in advertising with Corporate India, please don't hesitate to contact us. Our team is here to assist you with the process and answer any questions you may have. We look forward to the opportunity to work with you and help your business reach its full potential.

Fill out the form below to subscribe to our newsletter and never miss an update