Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Published: May 15, 2026

Updated: May 15, 2026

The no-holds-barred war between the US-Israel and Iran, now in its third month, has shaken the global economy, not least India. The immediate indicator of this economic quake is the country's stock market, with both the Sensex and Nifty50 falling sharply and wiping out over Rs 50 lakh crore of investor wealth.

India's Achilles' heel is oil import dependency, and with Brent crude shooting up to $ 115-120 per barrel, the country's fiscal indices have taken a beating with the rupee sliding to Rs 96.60 a dollar and importing inflation risk.

Sectorwise, the pain is being felt by oil marketing companies, capital goods exporters, and airlines as Indians shy away from foreign travel. As far as India is concerned, the 'villain of the piece' is the Strait of Hormuz.

India imports nearly 85-90% of its crude oil requirements and a large chunk of the global oil trade passes through the Strait. The Iranian regime's chokehold on Hormuz is threatening global, and particularly India's, energy supplies.

On February 28, 2026 morning after missiles flew across the Middle East, India's financial markets woke to a different world. The US-Israel strikes on Iran and the latter's retaliation jolted global risk appetite, pushed crude oil prices sharply higher and yanked the rupee down. Concurrently, the Indian stock market too came under the shadow of the West Asia war and, within a matter of weeks, Indian equities swung from persistent dip-buying to disciplined de-risking as geopolitics elbowed past earnings as the dominant driver of prices.

The outcome: a fast and broad de-rating. The Sensex, the most popular stock market index based on prices of 30 pivotal stocks quoted on the BSE, and Nifty50, the favourite index of analysts, based on 50 leading stocks quoted on the National Stock Exchange, tumbled down roughly 7% and 13% peak-to-trough through late March-early April, with an estimated Rs 50-57 lakh crore of market capitalisation erased before a partial bounceback.

The oil shock was the macro fulcrum. Brent shot up as high as $ 115-120 per barrel with a partial Hormuz Strait disruption, importing inflation risk into India and compressing equity risk premia.

Sharp depreciation in the currency and rates tightened financial conditions. The rupee slid to Rs 96.60 a dollar at the lows, while the 10-year government security yield moved up to 7%, raising discount rates for equities. Over 400 Indian stocks fell in double digits, and the sell-off spanned large, medium and small caps.

Sectorwise, the pain was felt by oil marketing companies (as crude oil prices shot up) airlines (as the Prime Minister urged citizens to reduce foreign travel), capital goods exports (as supply chains were disrupted) and interest rate-sensitive financial instruments.

The West Asia conflict, which started on February 28, has paused but not ceased, and the drums of war continue to echo through Dalal Street. The US-Iran war has emerged as the single biggest external threat facing the Indian economy and stock market in 2026.

Though India is not involved with any party in the war and the country is thousands of kilometres away from the Middle East battleground, the bloody conflict between the US and Israel on one side and Iran on the other has had a tremendous impact on the Indian economy, and consequently on the Indian stock market.

The obvious question that arises is: Why does Iran matter so much to the Indian economy? India imports nearly 85-90% of its crude oil requirements and a large chunk of the global oil trade passes through the Strait of Hormuz — one of the world's most strategically sensitive shipping routes. Any military escalation involving Iran immediately threatens global energy supplies.

HSBC expects India's earnings recovery to be delayed amid the impact of higher crude oil prices. Brent crude is up almost 40% since the Middle East war started in late February, and is currently trading around $110 a barrel, raising inflation and growth risks.

“Given India's reliance on imported energy and the potential knock-on effects on inflation and domestic demand, we are concerned about the durability of the ongoing earnings recovery,” said the brokerage. India is the world's third largest oil importer.

It added that the ongoing Middle East conflict has refocused attention on downside growth risks. While growth has shown signs of improvement in the last two quarters, HSBC now thinks the recovery from hereon will be delayed.

HSBC said the Indian government is likely to revise retail petrol and diesel prices upwards once state elections conclude, as energy prices are likely to remain elevated in the months and will result in a renewed rise in inflation, which could “undermine the gradual recovery in demand and contribute to higher non-performing loans (NPLs) across the lending sector, creating downside risks to 2026 earnings.”

It expects consensus forecasts to be revised down in the coming months from current expectations of 16% YoY for 2026.

Though the Indian stock market's valuations have corrected meaningfully from their peak, they might appear elevated as earnings downgrades feed through, HSBC added.

It also highlighted concerns among foreign investors, particularly the risk of rupee depreciation if oil prices remain high, alongside rising worries about the impact of Artificial Intelligence on India's software services sector. Foreign portfolio investors have already sold $20 billion worth of Indian equities in 2026 so far, following net outflows of $18.9 billion in the whole of the previous year.

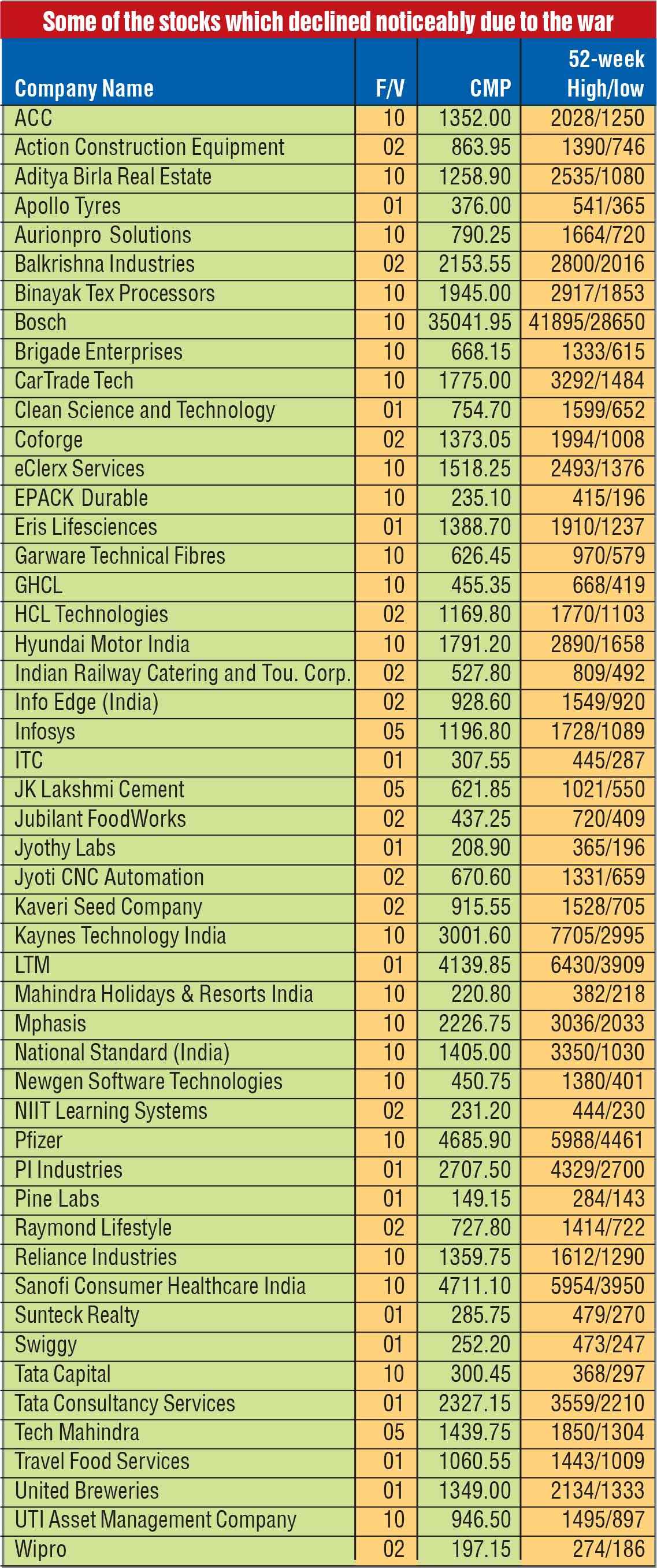

The West Asia war has hit the Indian economy very hard, resulting in weakening the Indian currency. Rising bond yields and costly crude oil have pushed up the current account deficit, have aided an inflationary price spiral and have triggered a broad market sell-off. Foreign institutional investors and foreign portfolio investors have continued offloading their stocks, pushing up foreign capital outflow to over $ 20 billion from February 28 till now. The Sensex, which was at a 52-week high of 85,883.50, tumbled to 75,317.92 and Nifty50 slided from 26,373.20 to 23,668.35. Individually, the Tata Consultancy Services (TCS) share price slided from Rs 3,559 to Rs 2,387 and Tech Mahindra from Rs 1,850 to Rs 1,440, HCL Technologies moved down from Rs 1,770 to Rs 1,170, Infosys from 1,728 to Rs 1,196 and Keynes Technologies from Rs 7,705 to Rs 3,002. Clean Science and Technology crashed from Rs 1,599 to Rs 755, Hyundai Motors to Rs 1,849 and Raymond Lifestyle from Rs 1,414 to Rs 727.

Global brokerage HSBC has doubled down on its bearish view on the Indian equity sector, downgrading it twice in less than a month as it sees the US-Iran war clouds and the subsequent oil price spike denting earnings recovery.

In a report dated April 23, HSBC downgraded India to ‘underweight’ after changing its stance to ‘neutral’ from ‘overweight’ on March 31. At the same time, it raised its stance on Korean equities to ‘neutral’, adding, “We fund our Korea upgrade by downgrading India.”

Analysing the stock market's performance during the US-Iran war, Ajay Bagga, a banking and stock market expert, said the Indian stock market is getting slammed by higher oil prices, a weakening balance of trade, a current account deficit and a sharply depreciating rupee. Pointing out that “global markets remain under pressure due to continued energy supply chain disruptions caused by the war,” he added that global markets are muted on the back of the energy supply crisis. Bond yields across the US, Japan, Europe, the UK and India are rising in reaction to rising inflation and in anticipation of inflation becoming anchored.

According to him, Nvidia results will be watched closely for pointers to the strength of the momentum — AI trade has been the bright spot in otherwise challenged markets. Meanwhile, the Indian rupee opened at a new low of Rs 96.88 against the US dollar while Brent crude oil prices remained elevated at $ 110 per barrel.

Other Asian markets also traded under pressure. Japan's Nikkei declined 1.59% to 59,590, Singapore's Straits Times Index was down 0.82% at 5,031, Hong Kong's Hang Seng dropped 0.65 per cent to 25,637, and South Korea's Kospi Index fell 2.42 per cent to 7,095.

On account of the US-Iran war, there has been an adverse impact on the stock market sentiment in India. That apart, other sectors have also been administered a body blow. One of the worst-hit sectors is aviation. Indian carriers face immediate pain because aviation turbine fuel (ATF) costs have surged with rising crude oil prices. As a spurt in ATF costs adversely affects their profit margins, these companies have no alternative but to raise ticket prices. This in turn has reduced air travel demand.

At the same time, as the balance of payments of the country is being hit on account of a sharp reduction in foreign exchange reserves, the Prime Minister has asked the public to reduce foreign travel. It is possible that, going forward, there will be restrictions on foreign travel by government officials. Thus, difficult days are ahead for aviation companies and this will obviously be against the interests of their shareholders. Investors may lose interest in stocks like Interglobe Aviation and SpiceJet.

Oil marketing companies will also face severe difficulties. Government-owned PSUs will be hard hit as crude oil prices shoot up, and OMCs will have to face margin erosion as fuel price hikes are delayed for political reasons, with the government imposing price controls. Consequently, OMC stocks will suffer a marked setback.

Paints, tyres and chemicals companies depend heavily on petroleum derivates. The crude price spurt will raise the cost of raw materials for these industries, placing pressure on their profit margins. All paints, tyres and chemicals companies will be in a vulnerable position on account of expensive raw materials, which will adversely affect their profitability. In a competitive environment, their pricing power will be weakened. As stock market prices are directly related to the financial performance of companies, shareholders in this sector will suffer on account of reduced dividends and other benefits.

The pace of growth of the automobile industry may slow down as it faces a double squeeze. Because of the crude oil price rise, various inputs will face an inflationary trend and prices of steel, aluminium and tyres will escalate. At the same time, freight costs will also go up. On the other hand, on account of rising inflation, consumer demand for automobiles will go down.

Of course, in a geopolitical crisis, not every sector turns a loser. In fact, this environment could be a golden opportunity for the defence sector and this could be good news for shareholders of defence companies. Wars and geopolitical tensions invariably increase military spending globally, and companies like Hindustan Aeronautics, Bharat Electronics and Bharat Dynamics could reap dividends in such a scenario.

History shows that geopolitical sell-offs often create the next generation of market winners — provided investors understand where the risks lie and where capital is likely to rotate next. Most people think war is bad for the stock market but this is not entirely correct. For some sectors, they may be a blessing. Clearly, the first sector to benefit greatly from wars is defence. Little wonder that during March 2026, while the Nifty50 index slumped by 11 per cent, the Nifty India defence index rose more than 6 per cent. While many sectors, including paints, tyres and chemicals, are bleeding, defence companies and their shareholders are in a cheerful mood.

This is quite understandable since countries at war need defence materials like planes, missiles, radar systems and ships, and spend billions in buying these items. Just think of India. In the wake of the border hostilities with Pakistan and China, India's defence budget for fiscal 2027 was as high as Rs 85 lakh crore — a record-breaking allocation in 79 years of independence.

Other countries have also started spending more on defence. Little wonder, exports of defence products from India are on the rise. During fiscal 2025, India's defence exports grew to about Rs 23,000 crore and the government has now set a target of Rs 50,000 crore in exports by fiscal 2029. This means that Indian defence companies have remarkable growth prospects going ahead. The ongoing conflict in West Asia could increase this further by opening up big export opportunities. In March 2026, Indonesia signed a deal with India to buy the Brahmos missile system — one of India's biggest ever defence export deals. Little wonder, even in an environment of bloody military conflicts in parts of Asia, Indian defence companies and their shareholders are in a happy mood.

Reflecting this cheerful mood, the stock price of Bharat Dynamics moved up from Rs 1,240 on the day before missiles started flying in the Middle East to Rs 1,315 today, with Hindustan Aeronautics shooting up from Rs 3,984 to Rs 4,370, MTR Techno from Rs 3,686 to Rs 8083, Data Patterns (India) from Rs 3,071 to Rs 3,970, Astra Microwave from Rs 954 to Rs 1,175 and Apollo Micro Systems from Rs 239 to Rs 355.

Another sector that stands to benefit from the current hostilities is the upstream oil and gas producing companies like Oil and Natural Gas Company and Oil India Ltd, among others. As the supply chain has been disrupted, crude oil and gas prices have shot up. Brent crude, which was around $ 65 per barrel before the war started, has spurted to cross the $100 mark. Experts believe that if the hostilities persist, oil prices may even hit $ 200 a barrel. The spurt in global oil prices is bound to benefit Indian companies, with rising prices pushing up their profitability. Though such a price spurt may be a curse for oil marketing companies, it is a blessing for oil producing companies.

Another sector that will benefit from the current hostilities is precious metals like gold and silver, which are considered a safety blanket. When people panic because of war, an economic crisis or political instability, they rush to buy gold. Widespread and rising demand for precious metals has led to higher prices. This has happened again and again in history. Gold prices rose 7.5 per cent in six months after the Gulf war in 1991. It gained 5.9% after the 9/11 attacks in 2001. It rallied 8.2% in the first month after the Russia-Ukraine war started in 2022. In India, the numbers are even more striking. Gold prices climbed from Rs 82,450 per 10 grams in 2025 to over Rs 1,63,000 by early 2026, almost doubling in one year, driven mainly by global tensions and panic buying.

Sectors like pharmaceuticals and FMCG (fast moving consumer goods) mostly remained relatively insulated during the March 2026 market chaos, even as aviation, paints, bank stocks and chemicals fell sharply.

According to experts, the trajectory of the Indian stock market hinges heavily on the evolving geopolitical landscape and several key financial indicators:

1. The Path of Crude Oil:

If the conflict prolongs, sustained crude spikes will negatively impact FY27 corporate earnings. However, if diplomatic solutions de-escalate tensions, energy prices may stabilize, allowing markets to focus on India's strong structural domestic growth.

2. Domestic Resilience (The Buffer):

India's structural tailwinds remain a stabilizing force. Robust domestic institutional investor (DII) flows and strong retail participation have historically acted as a crucial cushion against massive FII sell-offs.

3. What to Watch:

Energy Costs: Keep an eye on global crude benchmarks (e.g., Brent crude) to measure inflation and corporate margin impacts.

Capital Flows: Monitor FII and DII activity as a barometer for market liquidity.

Safe Havens: Defensive sectors like Pharma and FMCG, as well as export-oriented sectors, are often watched as safe havens during Middle East crises.

Ergo, as stated earlier, there's clearly pain but there can also be gain for the stock market, corporates and investors, even as peace is a desired outcome for people globally.

May 31, 2026 - Second Issue

Industry Review

VOL XVII - 09

May 16-31, 2026

Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Lighter Vein

1 Year *

Subscription

Rs 1800 /-

3 Year *

Subscription

Rs 5000 /-

5 Year *

Subscription

Rs 8000 /-

5

International

Subscription

$ 99.99

Read Corporate India and add to your Business Intelligence

Popular Stories

A modern-day enigma and a ramification of humanity's never-ending advancements, e-waste refers to the scum con- cealed by the outward glow of ever-advancing technology.

Archives

Office Address

Unit No. 405, 4th floor, Madhu Industrial Park, Avadh Narayan Tiwari Marg, Mogra Village Road, Andheri (East), Mumbai – 400069.

Call/Whatsapp

If you are interested in advertising with Corporate India, please don't hesitate to contact us. Our team is here to assist you with the process and answer any questions you may have. We look forward to the opportunity to work with you and help your business reach its full potential.

Fill out the form below to subscribe to our newsletter and never miss an update