Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Published: May 31, 2026

Updated: May 31, 2026

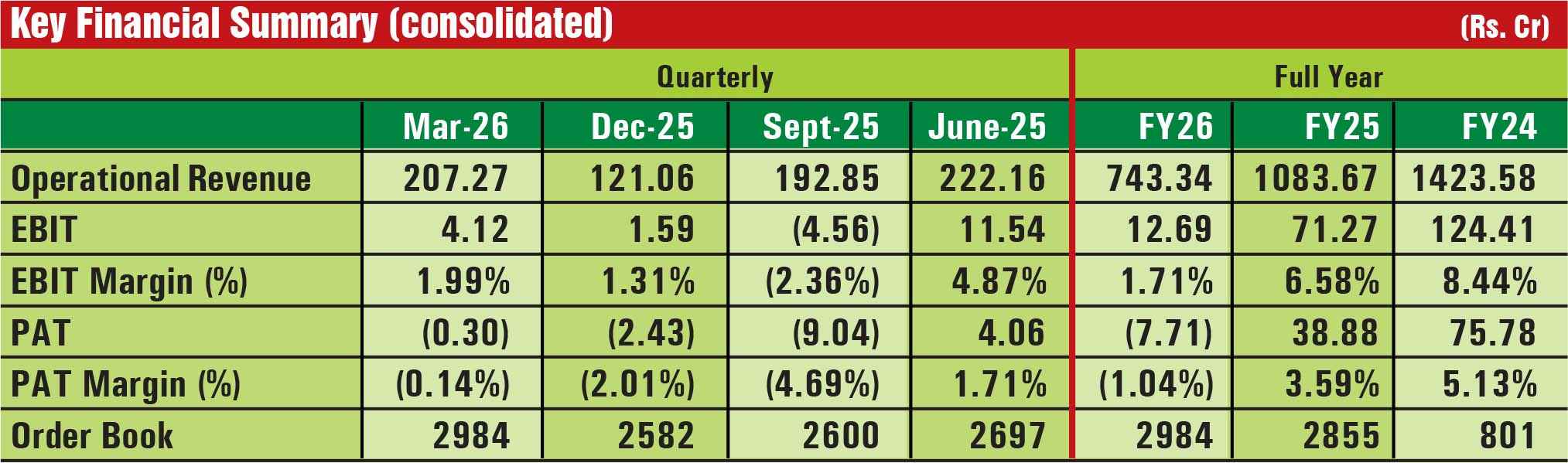

Based in Bangalore, DCX Systems, an NSE-BSE listed defence manufacturing player, has reported lacklustre financial results for FY 26. Operational revenue has gone down by 31.41% from Rs 1,083.67 crore in FY 25 to Rs 743.34 crore, EBIT by 82.19% from Rs 71.27 crore to Rs 12.69 crore, and PAT by -119.83% from Rs 38.88 crore positive to Rs 7.71 crore negative. Likewise, EBIT and PAT margins registered de-growth from 6.58% to 1.71%, and from 3.59% positive to 1.04% negative, respectively.

The management has attributed one of the blows to PAT to a Rs 16.27 crore loss incurred on foreign currency transactions. In another development, the company's Israel-based wholly owned subsidiary, Niart Systems Ltd, has reported a Rs 41.78 crore loss during FY 26, which is towards the cost of development of a product where commercial production is yet to commence. Hence, this particular expenditure has been recognised as capital expenditure and has not been taken into the P&L account. Otherwise, the net loss for FY 26 would have widened from Rs 7.71 crore to nearly Rs 50 crore. The management has not explained to how such a sizeable developmental expenditure would benefit the company's overall revenue and profits, moving forward.

Another wholly owned subsidiary of the company, Raneal Advanced Systems Pvt Ltd (RASPL), is growing rapidly as a state-of-the-art electronics manufacturing services (EMS) provider. RASPL operates out of a 40,000 sq ft world-class facility located in the high-tech defence & aerospace park in Devanahalli, Bangalore. It operates as an engineering and production resource, handling complex build-to-spec and build-to-print electronic products, and focuses on high mix, flexible volume and high complexity integrated electronic manufacturing. Raneal features highly specialised advanced surface-mount technology infrastructure. A standout feature introduced early this year is its over-sized PCB (printed circuit board) assembly line, capable of handling large-dimension and high-density boards up to 55 inches in length.

This unique manufacturing capability primarily serves mission-critical defence backplane applications, advanced power systems and large-scale industrial electronics. In addition, Raneal does several other important things as well. It's certain that this particular subsidiary will play a more important and significant role in the next phase of growth of the company.

DCX and ELTA Systems Ltd (a subsidiary of Israel Aerospace Industries) have formed an Indian joint venture company named ELTX Systems Pvt Ltd, which operates under an ownership model wherein ELTA holds a 63% equity stake and DCX holds the remaining 37%. The total investment is estimated at Rs 850 crore.

In May 2026, the joint venture officially broke ground for a state-of-the-art radar manufacturing, integration and testing plant. The new facility will come up in Tamil Nadu, taking advantage of the region's expanding defence industrial corridor. Construction is scheduled to be completed in April 2027, with commercial production and system testing soon thereafter.

Interestingly, ELTA Systems has granted an exclusive licence to the JV to utilise its proprietary radar technologies within India. The aim is to shift India from being an importer of Israeli systems to a self-sufficient co-developer. Though DCX would benefit only to the extent of 37% (coterminus with its stake), it is equally true that this partnership has provided an important opportunity to the company to explore manufacturing of select components in its own plant independently to supply to the JV company. Eventually, its widening role, strengthening capabilities and due recognition in the rapidly growing defence and aerospace domain will be beneficial in the long term.

DCX has recently been successful in demonstrating its Counter-Unmanned Aerial System (C-UAS) to the Indian Army, with technology from ELTA Systems Ltd Israel. The company is seeing increased opportunities to participate in the RFI/RFPs from the Ministry of Defence for surveillance and EW systems for securing new orders.

It is worthwhile highlighting that throughout FY 26, the company's order book position has remained encouraging (between Rs 2,600-3,000 crore), as it secures orders from domestic and international customers of high repute at regular intervals. However, its low EBITDA margin and poor PAT have raised questions about its earning capabilities. Clearly, merely operating in a critical and hi-tech domain will not make public and institutional investors happy unless the operational revenue grows consistently is supported by good operating margins and cash generation, as with other good players in a similar field.

The company has not been very successful in impressing potential investors, as its performance has been dismal in the last three quarters of FY 26. Commenting on the Q4 results, Dr HS Raghavendra Rao, CMD, said, “On a standalone basis, the company delivered improved operational performance and healthier margin levels during the quarter, compared to the preceding quarter. However, on a consolidated level, EBIT and PAT declined, primarily due to the incorporation of financial results of our subsidiary, NIART Systems, which is currently a product-based R&D entity and is yet to commence commercial production.”

Post the IPO of Rs 500 crore in November 2022, DCX Systems's equity capital was Rs 19.34 crore (Rs 2 face value), wherein the promoter group was holding 71.73%. In contrast, as of March 2026, it is now reduced to 52.16% in the enhanced equity capital of Rs 22.28 crore, which is quite substantial and disturbing from public shareholders' perspective.

In another fund-raising move through the QIP route in January 2024, the company raised Rs 500 crore from the non-promoter group at Rs 341 per share. Almost five months later in June 2024, the promoter group sold a small stake in the open market at an average price of Rs 355-358 per share. Some other stake dilution took place by effecting the structural reduction by a promoter group company, VNG Technology Pvt Ltd, over a scheme of amalgamation/arrangement/merger. Again, during the March-June 2025 quarter, they sold another lot whereby their net cumulative shareholding eventually dipped significantly from 56.85% to 52.16%.

Comparing the post-IPO December 2022 shareholding pattern with March 2026, it can be concluded that institutional holdings have gone down over time and individual resident shareholders who were merely 67,340 in number rose sharply by over 135% to 1,58,593 and in percentage terms from 11.68% to 36.58%. The stock, which got listed in November 2022 with a strong debut at Rs 287 against its issue price of Rs 207, has an all time high-low of Rs 451.90 (3.7.2024) and Rs 138 (2.3.2023).

In another thought-provoking and eye-opening exercise (with AI assistance), it is learnt that the weighted average cost of shares acquisition of the major promoter group entities ranges between 50 paise and Rs 5.65, whereas the IPO and QIP were priced at Rs 207 and Rs 341 per share respectively, not to talk of huge profits realised through offloadings in the secondary market. As a result, investors obviously feel they have been cheated, as the promoters have done everything legally, but not morally, in the eyes of public shareholders.

Now is the time for the promoters to reward shareholders, who have not received any dividend so far, so as to prove their integrity and commitment to the genuine and robust growth of the company.

The company came with an IPO to raise Rs 500 crore (including an Offer for Sale of Rs 100 crore) in the last quarter of 2022 at Rs 207 per share of Rs 2 face value. The equity capital is Rs 22.28 crore wherein the promoter group holds 52.16%. The book value per share is Rs 135.80, which certainly looks attractive vis-à-vis its current market price of Rs 191 and market capitalisation of Rs 2,129 crore. It also enjoys a debt-free-cum-cash surplus status. As of March-end this year, the inventory level is on the higher side at Rs 536.98 crore against Rs 288.97 crore a year ago, which suggests that certain despatches could probably take place in the current (April-June) quarter of the new financial year. Hence, one can anticipate improved revenue in the current Q1.

Undoubtedly, the company is operating in the highly promising and bright verticals of defence and aerospace, which have offer enormous opportunities to domestic players in line with their capabilities. Moreover, DCX has its own proven manufacturing competency in electronic systems, sub-systems, cable & wire harness assemblies and PCBAs. Further, its encouraging initial successful entry into counter-Unmanned Aerial System and the ambitious upcoming joint venture manufacturing with ELTA Systems, Israel for advanced radars certainly augurs well. Of course, the key to success lies in a seamless performance with reasonably good operating margins on a sustainable basis, which will attract potential investors.

At the current market price of Rs 191, the downward risk looks limited. Any new large order and/or improved EBITDA and net profit margins QoQ could trigger an upside to the stock price. However, we suggest entering the stock with a small quantity and accumulating later on reviewing new and positive developments, as the company has the potential to reward investors.

May 31, 2026 - Second Issue

Industry Review

VOL XVII - 09

May 16-31, 2026

Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Lighter Vein

1 Year *

Subscription

Rs 1800 /-

3 Year *

Subscription

Rs 5000 /-

5 Year *

Subscription

Rs 8000 /-

5

International

Subscription

$ 99.99

Read Corporate India and add to your Business Intelligence

Popular Stories

A modern-day enigma and a ramification of humanity's never-ending advancements, e-waste refers to the scum con- cealed by the outward glow of ever-advancing technology.

Archives

Office Address

Unit No. 405, 4th floor, Madhu Industrial Park, Avadh Narayan Tiwari Marg, Mogra Village Road, Andheri (East), Mumbai – 400069.

Call/Whatsapp

If you are interested in advertising with Corporate India, please don't hesitate to contact us. Our team is here to assist you with the process and answer any questions you may have. We look forward to the opportunity to work with you and help your business reach its full potential.

Fill out the form below to subscribe to our newsletter and never miss an update