Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Published: May 31, 2026

Updated: May 31, 2026

Situated 152 nautical miles from Nhava Sheva Port in Mumbai, Gujarat Pipavav Port (GPPL), widely known as APM Terminals Pipavav, is India's first seaport developed under a Public-Private Partnership (PPP) model. It functions as an all-weather, deep-draught, multi-commodity port located in Amreli district on the southwest coast of Gujarat.

The port acts as a vital ‘Green Gateway’, linking international maritime lanes with the heavily industrialised northwestern hinterland of India through efficient rail and road infrastructure. It features a 4,550 metre-long marine channel offering day and night navigation for all standard container, bulk, and RoRo vessels (LPG vessels are restricted to the daytime).

The fully integrated port with a multi-cargo terminal primarily supports four cargo verticals — Container, Dry Bulk, Liquid Bulk and Roll on/Roll off (RoRo), with an annual design capacity of 1.35 million TEUs, 4-5 million metric tons, 2 million mt, and 2,50,000-5,00,000 vehicles. Pipavav was the first port in India to establish a public-private railway partnership via Pipavav Rail Corporation (PRCL) and initiated India's first double-stack train services to double container transport capacity.

Apart from enjoying all weather-cum-multicommodity status, Pipavav port's significance is magnified by its direct integration with the western dedicated freight corridor (DFC) and the national hinterland. It's the first Indian port to gain this connectivity. Through PRCL, it provides 269 km of direct broad-gauge rail connectivity to the DFC at Mehsana and Ahmedabad. This reduces cargo transit time to the NCR and northwestern industrial modes by up to 50%. This positions the port as a primary gateway for raw materials and finished goods moving along the highly industrialised Delhi-Mumbai Industrial Corridor (DMIC). It's worth mentioning that DMIC is a massive ongoing mega infrastructure and industrial development project spanning six states — Uttar Pradesh, Haryana, Rajasthan, Madhya Pradesh, Gujarat and Maharashtra.

The port connects with world's top ten global container ports and eight of the top ten global shipping lines, and has consistently been ranked as India's most efficient port by the World Bank's Container Port Performance Index. Most importantly, Maersk, GPPL's parent organisation, is a leading, well-established organisation and among the world's top five shipping liner groups, also driving India's import-export volumes through its mega carriers.

APM Terminals Mauritius Ltd (a part of the Maersk group), manages and operates GPPL, with a 44.01% controlling stake. The total land area is spread over 1,561 acres. However, currently the port has been developed over 485 acres. Hence, the company will not need to acquire any new land for its expansion — around 1,000 acres of surplus land is a big positive.

The port is under a 30-year lease period from Gujarat Maritime Board which expires on September 29, 2028.

In 2025, the company entered into a non-binding MoU for a Rs 17,000 crore ($ 2 bn approx) investment to scale up the port's container, liquid and RoRo capacities, waterfront channel, container yard and rail-siding facilities. Of course, this is subject to getting a minimum extension period of 20 years.

The company is also building a three million tonne liquid jetty project at an investment of Rs 700 crore, expected to be completed by December 2026. It intends to start with one million tonnes in the next fiscal. Likewise, Swan Energy has advanced plans to establish LNG facilities within the Pipavav Port limits. The surrounding region is seeing massive investments in the energy sector. The adjacent Pipavav Shipyard (now Swan Corp) is also witnessing numerous big activities under its new management. The port serves as a primary logistical base for their project cargo, bulk materials and liquid gases. All these augur well for GPPL.

The Maersk group accords much importance to India and, seeing enormous growth opportunities, has long-term strategic plans to expand its operations in the country along with synergetic diversification. India also hosts Maersk's largest global workforce of 20,000 people. Recently, their group chairman AP Moller met Prime Minister Narendra Modi in Gothenburg, Sweden to elaborate on the group's investment plans in India's maritime sector, port automation, logistics corridors and upgradation of port infrastructure. They have also shown interest in accelerating green shipping solutions, adopting eco-friendly marine fuels and expanding India's domestic shipbuilding and repair capacities.

As a part of their $ 5 billion India investment plans, they have also signed an MoU to explore a suitable port investment opportunity of $ 1 billion to support Andhra Pradesh's port modernisation.

Undoubtedly, the parent company's strong presence, with a huge volume the world over supported by its unmatched ability to influence a wide customer base, augurs well for GPPL. Similarly, both the Centre and the Gujarat government are keen to have a bigger state-of-the-art port in the Saurashtra region, strategically located very nearly between Hazira on one side and Mundra-Kandla on other.

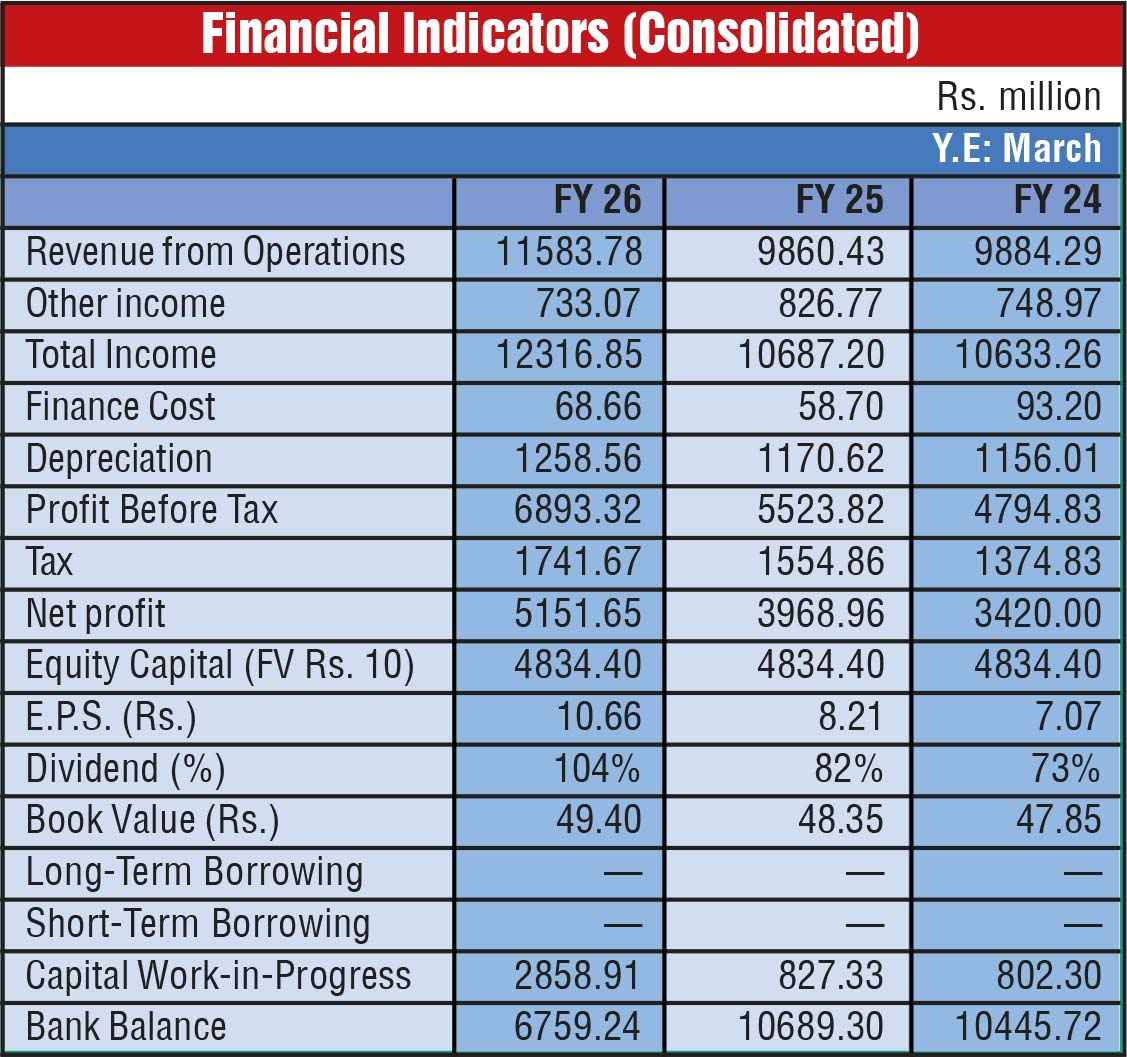

For the full FY 26, the company reported a 30% rise in consolidated net profit at Rs 515 crore, with operational revenue increasing by 17% to Rs 1,158 crore. Of late, a sharp surge has been seen in automobile cargo movement. The RoRo segment has emerged as the biggest growth engine for the port during the year, reflecting strong automobile exports. This particular segment's cargo volume jumped nearly 40% yoy to 67,000 units in the fourth quarter and 2,29,000 units for the full year, marking a 40% increase over FY 25.

The company expects RoRo volumes to rise 45-50% in the June quarter. To capitalise on rising vehicle exports, it is widening its infrastructure. “The RoRo staging area is on track and will be finished before the end of June. We are already doing 2,50,000 cars and now can easily handle 3,00,000-3,50,000 cars,” noted Managing Director Girish Aggarwal. A new pre-delivery inspection (PDI) facility being developed by NYK Line is expected to further increase capacity to 5,00,000 units.

The management expects a sharp shift in its cargo mix in the current June quarter due to the ongoing West Asia conflict, with liquid cargo volumes likely to fall 35-50% and bulk cargo volumes declining by 8-10% sequentially due to disruptions in movement of key commodities like fertilisers and LPG. Outlining this, Mr Aggarwal said, “One service which continues to not perform is the Middle East-Maersk service. Fertilisers, which largely come from the Middle East, was challenge in March and April. But we are seeing urea and other types of fertilisers coming back.”

Commenting on the LPG situation, Mr Aggarwal said, “LPG, which was muted in March-April, has started seeing growth. Now, a lot of LPG has started coming from the US, which has a longer travel time compared to the Middle East.” In a move to control expected damage in bulk and liquid cargo, the company expects container volumes to grow 5-7% supported by new shipping routes and shifting trade flows. Sharing emerging opportunities in transhipment, Mr Aggarwal explained, “We are trying to capture transhipment cargo handling which we did during April-May, helping to offset some of the disruption. Container growth is expected to be supported by Maersk's new F12 weekly service connecting Far East Asia with India, which includes Pipavav port in its route network. This service is starting early July and will start calling on Pipavav.”

Earlier, the National Green Tribunal (NGT) had dismissed an appeal against GPPL challenging the fresh environmental and CRZ clearances granted for the Rs 3,400-crore expansion project. Now, that has also been endorsed in the company's favour by the Supreme Court recently, and clears a major roadblock.

The million-dollar question troubling institutional and retail investors in the GPPL stock is: What if the Gujarat government does not give a lease extension of 20 years to APM Terminals? The existing promoter group has been operating Pipavav port (India's first PPP port) with an initial investment in 2001 and a controlling stake in 2005, and is now nearing the end of its 30-year concession agreement on September 29, 2028.

As the port is being operated under the Build-Own-Operate-Transfer (BOOT) policy, if an extension is denied the port assets will not automatically shut down. The real estate and waterfront structures will transfer back to the Gujarat Maritime Board. Relying on Supreme Court precedents regarding natural resources, GMB will put the fully developed, operational assets up for public auction wherein APM Terminals would also be eligible to participate as a fresh bidder. However, it would lose its grandfathered first-mover privileges and compete on tariff shares against deep-pocketed and keenly interested competitors like the Adani and Sajjan Jindal groups. The latter are currently the leading, aggressive and ambitious players in the ports and logistics domain, and would obviously be interested in having a strategically located, highly automated, well-operationalised and lucrative asset like Pipavav port in their fold.

Another, almost certain, effect of lease extension denial would be that APM Terminals will scrap its Rs 17,000-crore capital expenditure plans committed under the MoU with the Gujarat government in late 2025, because the MoU is non-binding and contingent on the lease's extension. Such a negative development could kill the company's valuation in the stock market. Then, both institutional and retail investors would rush to get out of the stock so as to either minimise their losses or control damage to potential gains.

This apart, the Maersk group might redirect its balance $ 3 billion India fund, committed to Indian maritime infrastructure, including alternative ports, which could be a big blow to the government's efforts to attract foreign investments. Moreover, this would also be seen as a bad precedent and send wrong signals to potential foreign investors, who would think twice before making any commitment, especially in domains involving natural resources.

Even as there is a strong possibility of GPPL getting through in the acid test of the 20-year lease extension, as a matter of precaution we feel it is prudent to highlight, with the assistance of AI, the inbuilt risk involved in the stock.

On equity capital of Rs 483.44 crore, the company has reported EPS of Rs 10.66 vis-à-vis Rs. 8.21 in the previous year. The book value for Rs 10 face value stands at Rs 49.40, whereas its debt-free status with cash surplus of Rs 994 crore and Capital Work-in-Progress of Rs 285.89 crore at year-end are quite positive. A dividend of Rs 5 per share (50%) has been proposed for FY 26.

The current market price of this NSE-BSE listed company is Rs 154.33, which converts the stock into a PE of 14.48 (Adani Ports & SEZ is being quoted at nearly 31 PE) with a market capitalisation of Rs 7,460 crore. The last one year's high-low are Rs 200 and Rs 141 respectively. Hence, the downside risk looks minimal. However, the ongoing West Asia war and geopolitical uncertainties are potential negative factors for the company in the short-medium term. At the same time, a very strong parent organisation (Maersk), its great interest in expanding and diversifying with deep roots in India, supported with an MoU of Rs 17,000 crore for GPPL, makes the stock worth watching-entering and accumulating gradually as the sector and the company both have a bright future and are capable of navigating any storm.

Nevertheless, a catch is that the company must get a 20-year lease extension from October 2028 onwards. Otherwise, the stock may not be worth buying for discerning investors.

May 31, 2026 - Second Issue

Industry Review

VOL XVII - 09

May 16-31, 2026

Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Lighter Vein

1 Year *

Subscription

Rs 1800 /-

3 Year *

Subscription

Rs 5000 /-

5 Year *

Subscription

Rs 8000 /-

5

International

Subscription

$ 99.99

Read Corporate India and add to your Business Intelligence

Popular Stories

A modern-day enigma and a ramification of humanity's never-ending advancements, e-waste refers to the scum con- cealed by the outward glow of ever-advancing technology.

Archives

Office Address

Unit No. 405, 4th floor, Madhu Industrial Park, Avadh Narayan Tiwari Marg, Mogra Village Road, Andheri (East), Mumbai – 400069.

Call/Whatsapp

If you are interested in advertising with Corporate India, please don't hesitate to contact us. Our team is here to assist you with the process and answer any questions you may have. We look forward to the opportunity to work with you and help your business reach its full potential.

Fill out the form below to subscribe to our newsletter and never miss an update